Langue

Internet leads can be great, but they can also eat up time. When every form that hits your CRM looks the same, it is hard to know who is serious, who can get approved, and who is just shopping on a lunch break. If your team is slow to respond or stuck in generic scripts, those leads cool off fast and many never turn into real appointments.

In this article, we will walk through how soft-pull credit tools help dealers move faster, personalize follow-up, and protect credit scores at the same time. We will look at what an automotive soft pull credit check really is, how it fits into internet lead follow-up, and how a credit-first process can turn more online shoppers into ready-to-buy customers.

Most stores see a flood of internet leads, especially around tax refund season, new model launches, and winter clearance events. On paper, that looks exciting. In practice, it often means:

• Slow response times when the team is stretched

• Low show rates for appointments

• Shoppers who stop replying after one or two messages

A lot of those leads are cold. They have not talked about budget, they have not talked about credit, and they are still sending forms to several other dealers.

Speed-to-lead is where the battle is won or lost. If you are not one of the first responses in their inbox or text thread, someone else will be. Soft-pull credit tools help here by letting you qualify a shopper in minutes without hurting their score. That means your team is not guessing. They can see who is ready, who needs more guidance, and who might be better for long-term follow-up.

With a credit-first sales platform that includes soft pulls, ID verification, trade values, and verified test drives, your workflow changes from “chase and hope” to “sort, plan, and act.” The rest of this article breaks down how that works.

Online shoppers move fast. Many will:

• Submit leads to multiple stores at once

• Expect a quick, helpful response, not just an automated email

• Keep scrolling if they do not hear back soon

When contact is delayed, a few things usually happen. You end up stuck in price-only talks, the shopper has already booked a test drive somewhere else, and your team is fighting from behind. By the time you finally connect, they may already be halfway through a deal at another store.

Fast response does more than just “get there first.” When that first touch includes real value, like:

• A clear payment range they might qualify for

• A sense of what lenders could fit their profile

• A ballpark trade-in value

you signal that you are serious, professional, and respectful of their time. That kind of quick, relevant info builds trust and gives you a better shot at earning their visit instead of being just another quote in their inbox.

There is a lot of confusion around credit pulls. Here is the simple breakdown.

A hard pull happens when a lender checks credit for a real approval. It can impact a credit score and will show up as an inquiry that other lenders can see. This is what happens later in the deal process when someone is ready to buy.

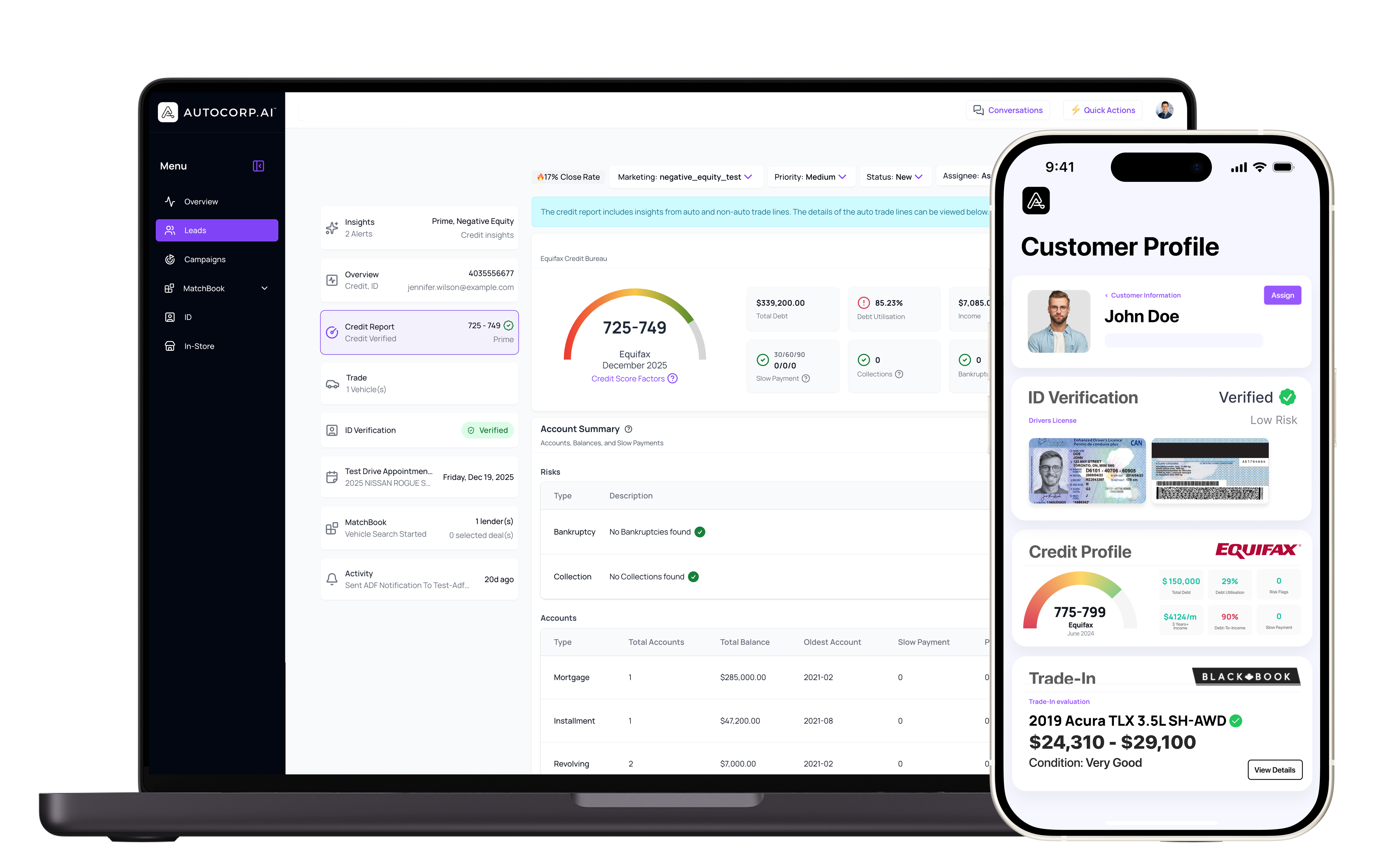

A soft pull is different. With an automotive soft pull credit check:

• The shopper’s score is not impacted

• It does not show up as a hard inquiry to other lenders

• You still get enough information to have a smart finance talk

Modern soft pulls usually give you a score range, a credit tier, and basic risk markers. It is not a full underwriting call, but it is more than enough to shape realistic options.

Consent and transparency are still important. Shoppers should know you are running a soft pull and that it will not hurt their score. When tools are built with privacy and data security in mind, F&I and compliance teams can feel comfortable using them as a standard step early in the process.

Once you have soft-pull data, your follow-up changes from one-size-fits-all to “this is actually about you.” BDC and sales teams can:

• Match conversation to likely budget and payment comfort

• Suggest vehicles that make sense instead of long-shot options

• Talk about approvals and buying power, not just “are you still shopping?”

With soft-pull tools built into a credit-first platform, your emails, texts, and calls can include real value like:

• Estimated payment ranges for the types of vehicles they viewed

• Rough lender fit, so you know which banks might work best

• Down payment guidance that is realistic for their situation

This kind of personalization lowers friction. Credit talks feel smoother because you are not springing it on them at the desk. Shoppers feel more confident, which makes it easier to move them from internet lead to in-store or remote test drive.

When every fresh lead looks the same, your team often ends up working in order, not by real opportunity. Automatic soft pulls on inbound digital leads flip that.

Now you can:

• Flag highly qualified buyers for immediate live contact

• Route borderline credit leads to a finance-focused specialist

• Place low-intent or low-readiness leads into long-term nurture

Operationally, this means your BDC is spending more time where there is real buying power. They can chase fewer ghosts, set better appointments, and improve show rates because they are inviting people who have already taken a real step toward approval.

When soft pulls sit beside tools like ID verification, trade-in valuations, and verified test drives in one platform, you get a clear picture fast. Managers can assign the right rep, pick the right follow-up plan, and move quickly while the shopper is still engaged.

Many shoppers are nervous about anything that sounds like a credit check, especially early in the year when they may be rebuilding or planning ahead. Soft pulls are a low-risk way to start the finance talk without damage to their score.

Strategically, soft pulls let you:

• Pre-qualify shoppers before triggering any hard inquiry

• Save hard pulls for customers who are deal-ready and serious

• Make better offers without over-promising or guessing

Clear, honest messaging helps here. Simple lines like “See your buying power with no impact to your credit score” put people at ease and encourage more leads to take that step. Once they do, your team has what it needs to guide them toward the right vehicle, the right lender, and the right appointment time.

Credit-first follow-up keeps things fast, personal, and respectful of the shopper’s financial health. Used well, it is good for your store and good for your customers.

Put qualified customers in the right vehicles faster with our streamlined automotive soft pull credit check solution. At Autocorp.ai, we help you surface real credit insights without impacting your shoppers’ scores, so they feel confident sharing information early in the journey. If you are ready to modernize your lead process and improve close rates, reach out and contact us today.