Langue

Most dealers do not have a traffic problem. The real problem is turning all those clicks and form fills into real people who show up, qualify for funding, and actually buy. When your team spends half the day chasing weak leads, everyone feels it, from the BDC to the F&I office.

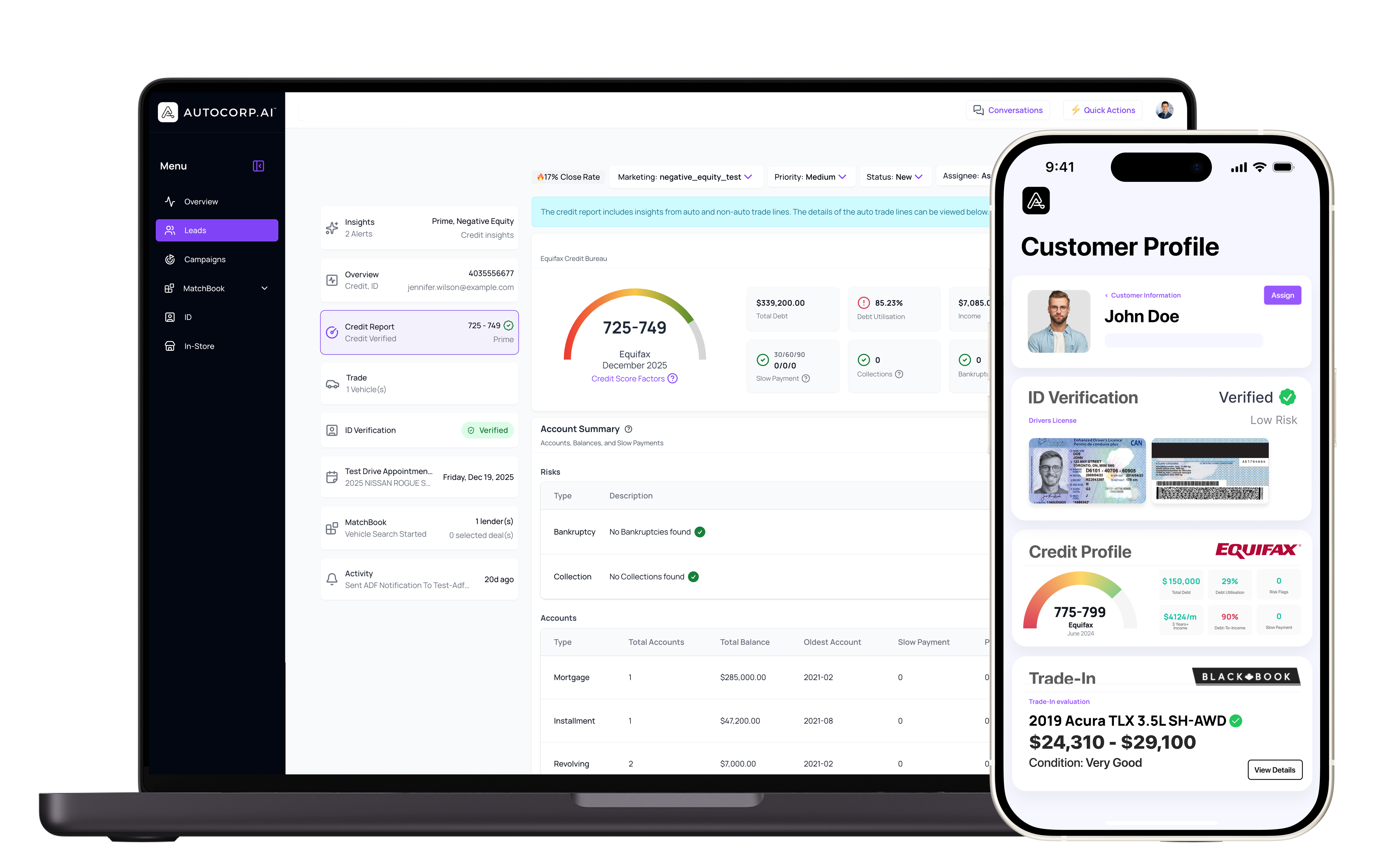

Credit-qualified leads software promises something simple: take anonymous visitors on your site and turn them into verified, finance-ready buyers inside your CRM. Instead of guessing who can really buy, your team works with clear credit insight, ID checks, trade info, and booked test drives.

Early spring is the perfect time to tighten this up. Tax refunds start hitting, new model promos ramp up, and RV and marine shoppers wake up as soon as the weather feels a bit nicer. In this guide, we will walk through how to design a credit-first workflow, keep compliance and trust tight, train your team, and plug a platform like credit-qualified leads software into your current CRM without blowing up your process.

Before you add any tool, get clear on the flow you actually want. A simple credit-first workflow looks like this:

• Website visitor clicks a payment or pre-qualification tool

• Soft-pull credit runs with clear consent

• ID verification confirms they are real

• Trade-in details are captured

• Test drive or appointment is booked

• F&I sees a clean, finance-ready profile in the CRM

The goal is not to bolt on “one more login” for your team. The goal is to weave credit-first steps into what you already do. That means:

• Updating BDC scripts to offer pre-qualification early

• Having sales managers review payment-ready deals instead of raw leads

• Making sure your internet lead rules still work, just smarter

Think across departments. Sales needs quick alerts when a hot, qualified lead hits. The BDC needs simple views and scripts that match those alerts. F&I needs enough credit and trade detail to structure deals without chasing missing info. When everyone knows where they touch the software in the process, the handoffs get smoother and the deal moves faster.

Once the workflow is clear, the next step is connecting the software to your CRM. Start by deciding which lead sources should run through credit qualification:

• Your main website forms and payment tools

• Third-party marketplace leads you want to prioritize

• Seasonal campaigns for tax refund buyers or RV and marine shoppers

Inside your CRM, set clear rules for how credit-qualified leads are tagged and ranked. For example, you might want:

• A “credit-qualified” status or label

• Different task plans for prime and subprime credit bands

• Routing rules for auto, RV, marine, and powersports so each team sees the right leads

Think about the data that should write back into the CRM record. Helpful fields often include:

• Credit band or tier, not a full report

• Trade-in details and estimated value

• ID verification status

• Top vehicle interests and payment expectations

Your CRM stays the single source of truth. The credit-qualified leads software becomes the intelligence layer on top, feeding in better data on credit, ID, trade, and test-drive bookings. Your team still lives in the CRM they already know; they just see richer, smarter lead profiles.

Any time you touch credit data, you are also dealing with compliance and trust. With credit-qualified leads software, you need to think about rules like FCRA, privacy consent, and how soft pulls differ from hard pulls. Soft pulls are great for early web steps because they do not impact credit scores, but they still require clear permission.

On your website, lead forms, and templates, your consent language should make three things very clear:

• What you are doing, like running a soft credit check or verifying ID

• Why it helps the shopper, like showing real payments or protecting from fraud

• How their data is stored and used inside your systems

Inside your CRM and software tools, tighten access control. Not everyone in the store needs to see credit bands. Use role-based permissions and clear audit trails so you can see who viewed or changed sensitive info.

Spring selling peaks can strain even good processes. Higher volume means more chances for mistakes or shortcuts. Automation helps here. When your system automatically applies the right disclosures, consent tracking, and routing rules, your team can focus on the customer in front of them, not on trying to remember legal steps.

A new workflow only works if your people are ready to use it. With a credit-first model, we want BDC and sales to lead with payments and pre-qualification instead of only price and inventory. The goal is to use credit insight to show real options, early, and keep expectations honest.

Plan training in layers:

• Kickoff workshops to walk through the new flow step by step

• Live role-play sessions based on spring campaigns and tax refund callers

• Quick-reference scripts for phone, email, and text

• Short video refreshers embedded in your CRM or learning system

Language matters here. Your team needs simple, reassuring phrases, like:

• “This is a soft credit check, it does not affect your score.”

• “This helps us protect you from ID fraud before you visit.”

• “If we know your credit range, we can lock in the best options before you drive down.”

Managers should watch a small set of core metrics to keep the new habits in place:

• Credit-qualified lead conversion rate

• Appointment set and show rates

• Time to first contact from the moment the credit-qualified lead hits the CRM

When you coach to these numbers in one-on-ones and sales meetings, the workflow stops being “extra work” and starts feeling like the normal way of doing business.

You do not need a huge project plan to get started. A simple 30-day rollout keeps things moving and low stress:

• Week 1: Map the workflow, review compliance, and lock in consent language

• Week 2: Connect the software to your CRM and test data flow on a small batch of leads

• Week 3: Train your team, update scripts, and finalize routing rules

• Week 4: Go live with one rooftop, or one department like internet or RV, and watch it closely

Starting with a pilot helps. Many dealers begin with online leads or a single segment like RV or marine. Once you prove that credit-qualified leads close better and move faster, you can roll the playbook out to the rest of the store.

Build a simple scorecard so everyone can see the impact:

• Number of credit-qualified leads created

• Close rate compared with non-qualified leads

• Gross per copy on deals that start with pre-qualification

• Time saved per deal because credit and ID are done upfront

Credit-qualified leads software, plugged cleanly into your CRM, sets your team up for the busy season with more verified, ready-to-buy customers instead of a pile of mystery leads. When your workflow, compliance, and training all work together, your salespeople spend less time chasing and more time closing.

If you are ready to focus your team on buyers who can actually get approved, our credit-qualified leads software is built to help you do exactly that. At Autocorp.ai, we use predictive credit insights so your BDC and sales staff spend less time chasing unqualified prospects and more time closing real deals. We will walk you through setup, integration, and best practices tailored to your dealership. Have questions about fit or implementation, or want a quick demo, just contact us.