In today’s competitive automotive retail landscape, the ability to engage, qualify, and convert leads faster can make all the difference. That’s where understanding the difference between pre-qualification and pre-approval becomes essential. For modern dealerships, especially those leveraging tools like AVA™ Credit, using both effectively can result in better customer experiences and more deals in the pipeline.

Let’s break down the key differences, benefits for dealerships, and how to use each stage strategically in your sales process.

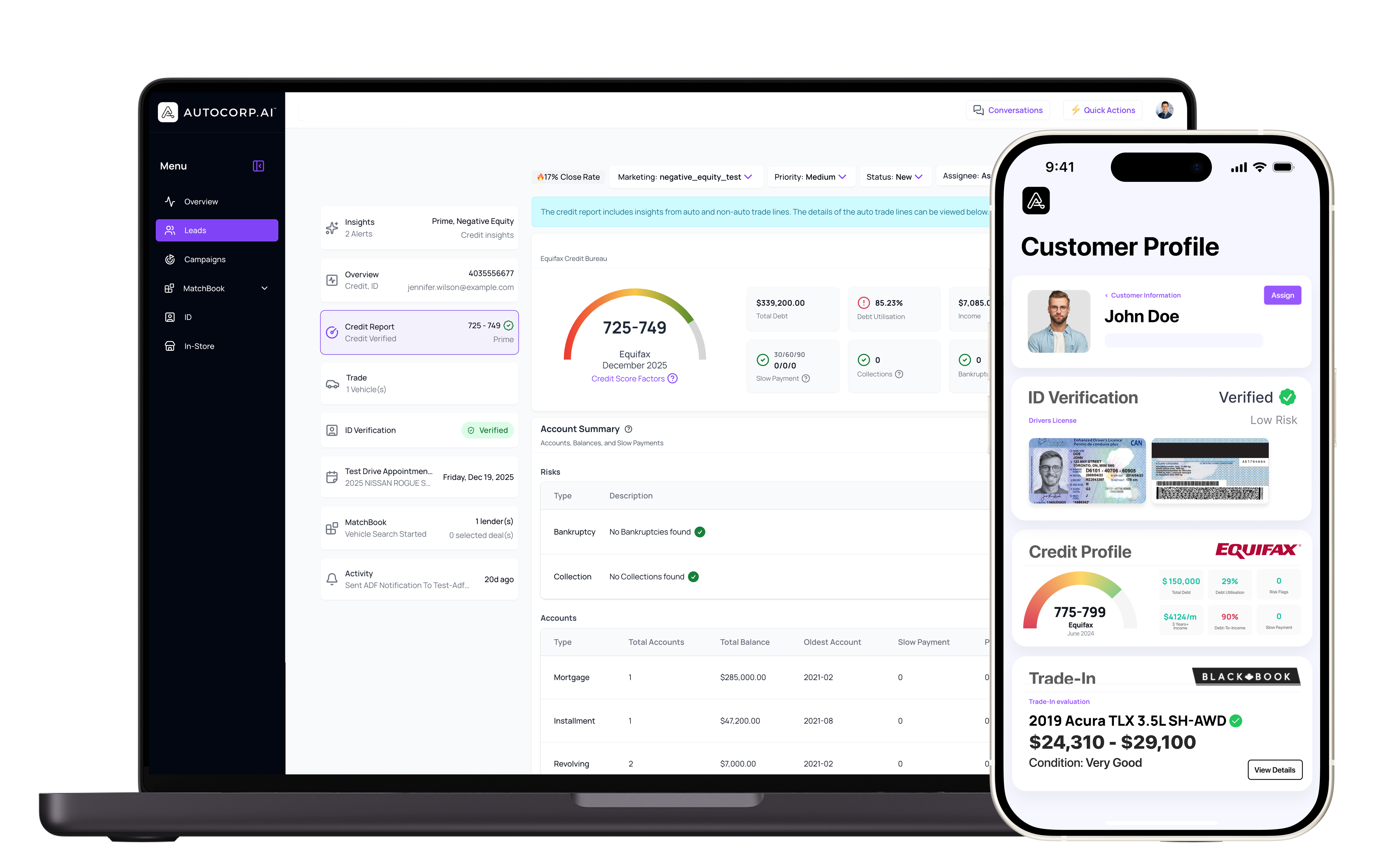

Pre-qualification is a quick, no-impact credit check that gives dealers an early view into a customer’s financial profile. It typically requires minimal information often just a name and contact info and can be completed online in seconds using soft pull credit technology like AVA™ Credit.

With AVA™ Credit, dealers can offer real Equifax soft pull credit checks right on their website. It allows shoppers to pre-qualify themselves before even stepping foot in the showroom, giving your team valuable insight before the first call or appointment.

Pre-approval is a formal financing process that involves a hard credit check. It requires more customer information, including SIN and proof of income, and typically involves selecting a lender and receiving a conditional approval for a specific amount or rate.

It’s not a matter of one or the other—offering both pre-qualification and pre-approval gives your dealership a strategic advantage. Think of pre-qualification as the front-end filter and pre-approval as the final step in your financing process.

When integrated into your CRM and digital retailing strategy, pre-qualification tools like AVA™ Credit help streamline the early sales process while feeding high-intent leads directly into your F&I pipeline.

Pre-qualification is an early look at a shopper’s buying power that uses a soft credit check. It gives estimated payment ranges without affecting the shopper’s credit score. Pre-approval is a formal credit decision that uses a hard credit check, which can impact the shopper’s score, and it confirms how much they can borrow and at what terms.

Pre-qualification uses a soft pull, so it does not affect a shopper’s credit score. That makes it a low-pressure first step for people who are nervous about their credit or not ready to apply. Dealers can use this to get better-quality leads without scaring off early shoppers.

Pre-qualification on a dealership website helps turn casual visitors into real leads. Shoppers get quick payment estimates without a hit to their credit, and dealers get richer data, such as income, budget, and credit profile. This helps sales and F&I teams start smarter conversations and reduces time spent with unqualified buyers.

Dealers should move a shopper from pre-qualification to pre-approval when the buyer has picked a vehicle or is close to a decision. At that point, a full credit application and hard pull make sense, since the dealer needs firm terms to desk the deal, lock in a lender, and prepare contracts.

Pre-approval gives dealers a confirmed lending decision, including amount financed, rate, and term. This removes guesswork in the showroom, helps desk realistic deals faster, and cuts down on rehashing with lenders. With solid numbers in place, buyers feel more confident, trust the process more, and are less likely to walk away.

Understanding the roles of pre-qualification vs. pre-approval is crucial for every dealership aiming to optimize its sales funnel and improve the customer journey. Pre-qualification helps you cast a wider net and build trust, while pre-approval closes the deal with confidence.

By offering AVA™ Credit on your website and in-store, you’ll create a smoother, more transparent path to purchase while boosting lead quality, team efficiency, and customer satisfaction.