Language

Spring hits and shoppers wake up. As soon as the weather starts to warm, people begin hunting for fresh rides, RV trips, boats for the lake, and powersports toys for the first clear weekend. Almost all of that early shopping starts online, and those same shoppers are bouncing between several dealer sites in one sitting.

On most of those sites, they hit the same thing: a basic form asking for name, email, phone, and maybe a “cash, or finance” question. That kind of form might grab contact info, but it tells the sales team almost nothing about who is actually ready to buy. It also does not give any real signal on credit or deal structure.

This is where the big decision comes in. Do you keep using simple question-based lead forms, or move to website credit form software that can pull soft credit, check identity, and line up a real finance path before the shopper walks in? The choice shapes lead quality, sales efficiency, lender fit, and how many spring shoppers you close before they move on to another store.

Question-based forms feel safe because they are familiar. But they leave huge gaps.

Here is what usually comes in from these forms:

• Name and contact info

• A preferred vehicle or stock number

• A loose idea of budget or down payment

• A checkbox about financing or cash

That is not enough to know if the deal has any legs. Your team is stuck guessing, then calling, texting, and emailing just to find out whether the shopper can actually be approved for the vehicle they picked. By the time you uncover a credit roadblock, you may have spent a lot of time on a deal that was never a fit.

These forms can also feel heavy for the shopper. Long lists of questions, income boxes, or vague “how is your credit?” fields cause people to bail. Credit-sensitive buyers, especially those who had trouble getting approved before, may shut down if they think a hard pull is coming or that they will be judged.

On top of that, lenders are not helped by this kind of lead. With no real credit insight up front, deals land on the desk that do not line up with lender programs. Desk managers end up reworking structures or turning deals down after a long back-and-forth. That slows the whole store and frustrates both staff and shoppers.

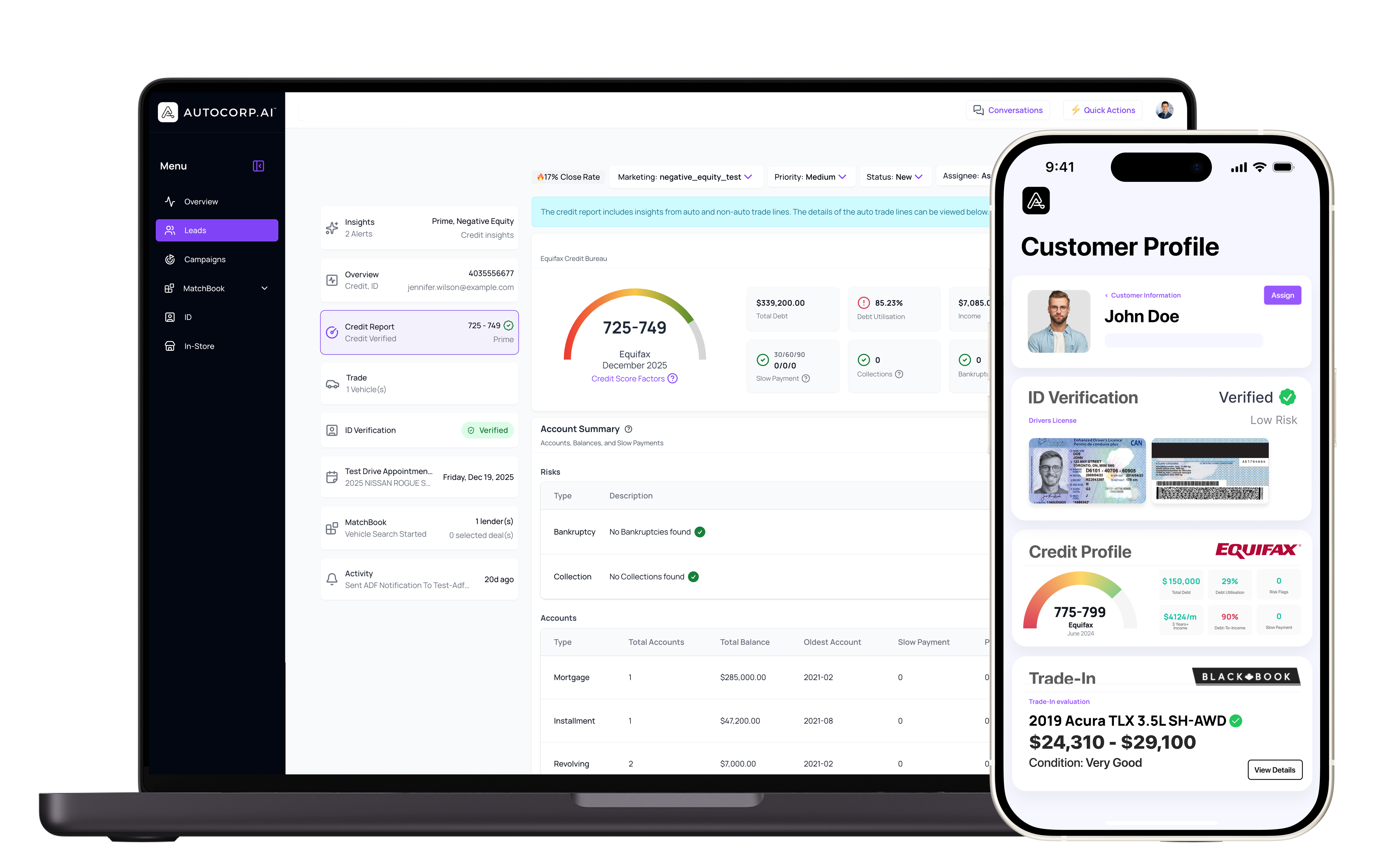

Website credit form software flips the order of the process. Instead of starting with loose questions and guessing at credit later, it brings credit insight into the very first online step.

Credit-first forms pull a soft credit report, so shoppers can share real information without a hard hit to their score. Now your team can see key credit details early, match the shopper to the right inventory, and think about realistic payments, all before the person steps on the lot.

Good credit-first flows also connect other tools in the same path, such as:

• ID verification and basic fraud checks

• Trade-in capture and valuation

• Simple consent and disclosures

• Test drive verification or check-in steps

All of this happens in one smooth online experience. Instead of several separate tools and forms, the shopper feels like they are completing one guided path that builds a complete, credit-first profile.

From the shopper’s side, this feels simpler and more honest. Clean screens, clear progress bars, and plain-language disclosures help lower stress. They get to share what the store actually needs, in a mobile-friendly format that works when they are on the couch, at work, or out by the driveway looking at their trade.

Once you put these two approaches side by side, the differences stand out quickly.

On lead quality versus lead volume:

• Question forms usually bring in more total entries, but many are tire kickers or unqualified.

• Credit-first forms may bring in fewer leads, but the leads carry real intent and real data.

• With credit insight attached, your team spends more time on people who can actually buy.

On time-to-deal versus time-to-chase:

• With basic forms, salespeople chase low-intent, low-info leads and try to “find the deal” after the fact.

• With credit-first flows, they can structure deals early, get quick readouts from lenders, and set stronger appointments.

• Desk managers get to work on deals that already fit lender guidelines instead of reworking weak structures.

Credit-first flows also pull your store together across departments. When credit data, ID checks, and trade values live in one connected system, sales, F&I, and management are working off the same picture. There is less rehash, fewer surprises in the box, and fewer awkward moments where the payment changes late in the process and the shopper cools off.

At Autocorp.ai, we focus on dealers in automotive, RV, marine, and powersports, including stores in regions where spring shoppers are eager to hit the road and water as soon as the snow melts. That means we design credit-first flows for a wide mix of buyers, from subprime to strong prime, and for a wide mix of inventory.

Our website credit form software brings key tools into one online stream:

• Soft-pull credit for upfront insight without score impact

• ID verification to help protect the store from fraud

• Trade-in capture and valuation inside the same experience

• Test drive verification so visits feel more organized

To the shopper, it feels like one clean form. To your team, it shows up as a structured, lender-ready opportunity. A visitor starts as an anonymous browser on a VDP or finance page, completes the credit-first flow, and turns into a ready-to-work file with credit, ID, and trade data tied together.

Now your sales and F&I teams can look at that profile, match the shopper to the right vehicle and lender, and move straight to setting a solid appointment. You are not just catching a lead, you are building the early version of a funded deal.

Spring traffic comes fast, and it is easy for stores to slip into “just collect more leads” mode. This is the time to pause and look at the forms on your site with a sharper eye. How many fields do shoppers have to fight through? How often does your team find out about a credit hurdle only after several calls or a long visit?

Switching from question-only forms to website credit form software is really a mindset change. It moves your focus from lead capture to deal creation. Instead of filling your CRM with low-info names, you are filling your pipeline with credit-ready shoppers who already fit a real finance path.

If you are ready to streamline how customers apply for financing, our website credit form software can help you capture more leads without adding extra steps to your process. We give your team the tools to pre-qualify buyers quickly while protecting their credit and personal information. To discuss how this fits your existing workflows, contact us and we will walk you through a tailored setup for your dealership. Autocorp.ai is focused on helping you turn more website visitors into confident, ready-to-buy customers.